Rent or Buy?

February 12, 2008 By Alan J. Salzberg

The answer to the age-old question, according to every grandmother out there, is "buy." But do the data really support this?

Housing as an Investment

Forgetting for the moment about the psychological advantages and disadvantages of buying versus renting, let's look at the Economics, and, of course, the probabilities.

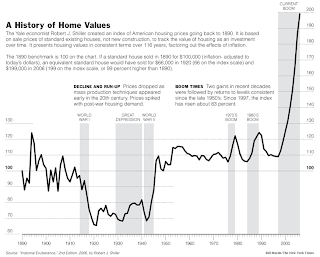

One of the most fascinating pieces of information to answer this question is a chart put together by Robert Shiller (Yale Economist) as part of his book Irrational Exuberance (he also has an article on the housing market with similar charts in Economists' Voice, March, 2006). Shiller looks at inflation-adjusted housing prices from 1890 to the present. I got the chart from this site, and the whole article is free and downloadable here (search on Shiller).

Shiller sets the price of a house in 1890 at 100, and shows how the value varies over time, adjusting for inflation. Thus, in 1947, soon after the war, the value is 110, 10% higher than in 1890. In 1989, the peak of the last boom, it is around 125. And now? Around 200!

Besides the obvious "irrational exuberance" of the housing market that is indicated in this graph, another interesting fact comes out: Housing goes up and down over time and in any given 20 or 30 year period, can be either a good investment or a bad one. Sure, if you timed the last couple of booms correctly, you could have made a killing, but the fact is that a house bought in 1960 was basically the same price in 1995, after accounting for inflation. Of course, the person who bought that house could have lived there for 35 years, paying only the cost of upkeep, and, presumably the mortgage.

Total Return to Renting Versus Buying

That brings us to the next topic: knowing that a house may or may not give you any real capital appreciation, is it better to buy or rent?

One of the big arguments I hear from my mother-in-law against renting is that "you are just throwing your money away." Seems like a good point. With renting, you get absolutely nothing out of it, but with buying, after 30 years, you own a house. The problem with this argument is it ignores two things: 1) the down payment, and 2) interest.

When you buy a house, you put around 20% down. That money then cannot be invested elsewhere. In addition, you pay interest on a loan, whose proceeds are invested in the house. The good thing is that you are using the proceeds from your loan to buy an asset 5 times the value of what you invested in cash. For example, if you buy a $500,000 house, you only have to pay $100,000. Thus, if you are in one of the boom times in Shiller's graph, you get 5 times what his graph shows in return on your $100,000 investment. The flip side, of course, is that in the bust times, you get 5 times the losses.

Compare this to renting. Here, you keep your $100,000, perhaps investing it in safe 5-year Treasury notes, where you can expect an inflation adjusted return of about 2.5% (see the fed site for T-note rates and the Bureau of Labor Statistics site for inflation rates--the real return is lower if you go back more than 40 years).

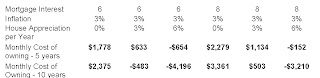

Now, let's look at renting or buying with specific numbers. Suppose that you have a $500,000 home in mind. For buying the house, your total costs are your mortgage and your return is the amount you get back after the sale, minus the $100,000 you paid as a down payment. For renting, your costs are your rent and your return is the cash you get in interest from your $100,000 investment.

The following table lays out 6 scenarios (click on the table to see a legible version). I've adjusted for the tax benefits of the mortgage as well as inflation.

I varied the mortgage interest rate and the (annual) house appreciation. The two numbers at the bottom are your out of pocket monthly costs after 5 and 10 years for owning the house. Presumably, this is the amount in rent you should be prepared to pay. Thus, for a house that appreciates at the rate of inflation (roughly what has happened with housing since 1890--it is the 3% appreciation in the 2nd and 5th columns), your monthly costs are $633 if you have a 6% mortgage and sell after 5 years and $1,134 if you have an 8% mortgage. You do much better if you hold the house for 10 years. Not true for the house that does not appreciate. Then, you do better if you hold it for less time.

To really answer the question well, we'd need an accurate prediction of inflation and mortgage rates. In the short term, both of these are pretty easy. The second thing you need is an idea of how long you will hold the house. If the house appreciates at the rate of inflation, then you are better off holding onto it for longer. If it does not, then you are better off selling sooner.

What is apparent is how radically the value changes depending on the assumptions about how much the house will appreciate. Put in some negative numbers and it really gets scary. If the current boom results in a 2% annual nominal depreciation over the next 5 years, then your 5-year monthly cost goes to about $2,500. At 5% a year depreciation (something that occurred over several years with NYC apartments in the early 90s), then your out of pocket is $3,500 per month if you sell after 5 years.

So, should you rent or buy?

Well...it depends.

Housing as an Investment

Forgetting for the moment about the psychological advantages and disadvantages of buying versus renting, let's look at the Economics, and, of course, the probabilities.

One of the most fascinating pieces of information to answer this question is a chart put together by Robert Shiller (Yale Economist) as part of his book Irrational Exuberance (he also has an article on the housing market with similar charts in Economists' Voice, March, 2006). Shiller looks at inflation-adjusted housing prices from 1890 to the present. I got the chart from this site, and the whole article is free and downloadable here (search on Shiller).

{kind=link}

Shiller sets the price of a house in 1890 at 100, and shows how the value varies over time, adjusting for inflation. Thus, in 1947, soon after the war, the value is 110, 10% higher than in 1890. In 1989, the peak of the last boom, it is around 125. And now? Around 200!

Besides the obvious "irrational exuberance" of the housing market that is indicated in this graph, another interesting fact comes out: Housing goes up and down over time and in any given 20 or 30 year period, can be either a good investment or a bad one. Sure, if you timed the last couple of booms correctly, you could have made a killing, but the fact is that a house bought in 1960 was basically the same price in 1995, after accounting for inflation. Of course, the person who bought that house could have lived there for 35 years, paying only the cost of upkeep, and, presumably the mortgage.

Total Return to Renting Versus Buying

That brings us to the next topic: knowing that a house may or may not give you any real capital appreciation, is it better to buy or rent?

One of the big arguments I hear from my mother-in-law against renting is that "you are just throwing your money away." Seems like a good point. With renting, you get absolutely nothing out of it, but with buying, after 30 years, you own a house. The problem with this argument is it ignores two things: 1) the down payment, and 2) interest.

When you buy a house, you put around 20% down. That money then cannot be invested elsewhere. In addition, you pay interest on a loan, whose proceeds are invested in the house. The good thing is that you are using the proceeds from your loan to buy an asset 5 times the value of what you invested in cash. For example, if you buy a $500,000 house, you only have to pay $100,000. Thus, if you are in one of the boom times in Shiller's graph, you get 5 times what his graph shows in return on your $100,000 investment. The flip side, of course, is that in the bust times, you get 5 times the losses.

Compare this to renting. Here, you keep your $100,000, perhaps investing it in safe 5-year Treasury notes, where you can expect an inflation adjusted return of about 2.5% (see the fed site for T-note rates and the Bureau of Labor Statistics site for inflation rates--the real return is lower if you go back more than 40 years).

Now, let's look at renting or buying with specific numbers. Suppose that you have a $500,000 home in mind. For buying the house, your total costs are your mortgage and your return is the amount you get back after the sale, minus the $100,000 you paid as a down payment. For renting, your costs are your rent and your return is the cash you get in interest from your $100,000 investment.

The following table lays out 6 scenarios (click on the table to see a legible version). I've adjusted for the tax benefits of the mortgage as well as inflation.

I varied the mortgage interest rate and the (annual) house appreciation. The two numbers at the bottom are your out of pocket monthly costs after 5 and 10 years for owning the house. Presumably, this is the amount in rent you should be prepared to pay. Thus, for a house that appreciates at the rate of inflation (roughly what has happened with housing since 1890--it is the 3% appreciation in the 2nd and 5th columns), your monthly costs are $633 if you have a 6% mortgage and sell after 5 years and $1,134 if you have an 8% mortgage. You do much better if you hold the house for 10 years. Not true for the house that does not appreciate. Then, you do better if you hold it for less time.

To really answer the question well, we'd need an accurate prediction of inflation and mortgage rates. In the short term, both of these are pretty easy. The second thing you need is an idea of how long you will hold the house. If the house appreciates at the rate of inflation, then you are better off holding onto it for longer. If it does not, then you are better off selling sooner.

What is apparent is how radically the value changes depending on the assumptions about how much the house will appreciate. Put in some negative numbers and it really gets scary. If the current boom results in a 2% annual nominal depreciation over the next 5 years, then your 5-year monthly cost goes to about $2,500. At 5% a year depreciation (something that occurred over several years with NYC apartments in the early 90s), then your out of pocket is $3,500 per month if you sell after 5 years.

So, should you rent or buy?

Well...it depends.